King County Reduced Cost Center Addition Lead Time By 40% With GLSS

This Case Study was originally published in November 2017.

Home » Case Study » King County Reduced Cost Center Addition Lead Time By 40% With GLSS

THE CHALLENGE

New projects for King County mean new grants and new cost centers. But setting up cost centers was taking too long and nothing could proceed without the new cost center. There were customers waiting over 30 days—and some 80 days—to have their forms processed. Megan Rulien, an Administrator at King County Finance and Business Operations Division (FBOD) decided to address the problem by turning it into a Lean Six Sigma project.

SOME BACKGROUND

King County—the most populous county in the state of Washington—includes Seattle, the most populous city. The Financial Business Operations Division (FBOD) handles all the finances for the county. That includes procurement, accounting, fund monitoring, and taxes. Megan points out, “Any way of bringing money into the county comes through us. It’s a big job for a big county.”

Cost Centers are used for budgeting and managing costs. When the county launches a new project or receives a new grant a cost center needs to be established. This helps denote it from other projects and grants in the system. The agency with the new project submits a request to establish the new cost center. Work starts once the new cost center is in place.

Megan interviewed the people working in the process and learned they believed it took far too long to process a new cost center form. It became obvious that the process was unclear. No one had mapped the process and there were no instructions.

Megan reviewed the past two years of cost center forms and learned it took an average of 7 business days to process a new cost center with some customers waiting months. Once Megan shared the information with the staff, they were not happy, but they were not surprised. They had a sense that it took too long. Until now no one had focused on the time it was taking to process these forms.

THE DISCOVERY

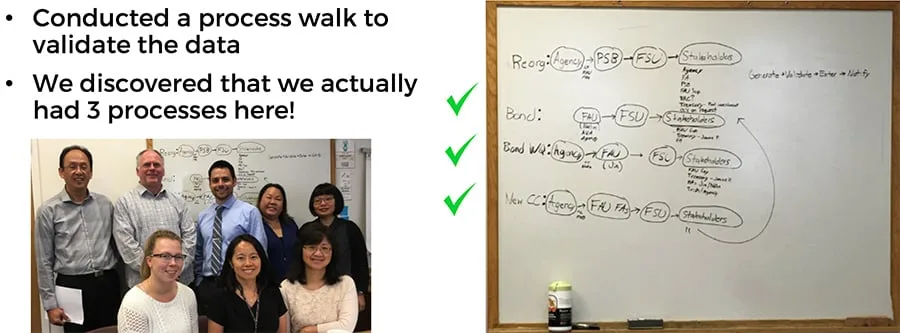

Megan and her team conducted a Process (Gemba) Walk and analyzed the existence of the 8 Wastes—Transportation, Waiting and Extra-Processing were the top contributors. But to their surprise, they also discovered there were three separate processes. Nobody knew this was happening.

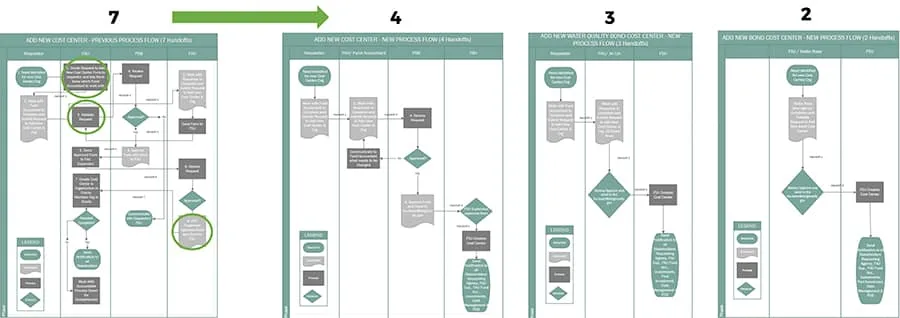

The three different processes related to different types of cost centers, one of them had more requirements and approval levels than the other two. All these years they had processed them as if they were all the same, applying the maximum levels of approvals and handoffs. The team quickly identified the two processes that didn’t need the extra handoffs and approvals. The process could be faster at least for these cost center forms. Together, they mapped out how the new processes should operate.

Next, Megan decided to figure out the biggest contributors to excess lead time. She calculated the correlation coefficients of various steps in the process in relation to the number of business days it took to create a new cost center. She found that over 93% of the variation in the time to add a new cost center was due to the supervisor having to approve the document. Other significant sources of variation included entering information and other approvals.

Megan is quick to point out that instead of pointing fingers at individuals they focused on the process. When she spoke with the supervisor, he revealed that the form was never wrong when it came to his desk. So why do this step?

Megan and the team reviewed the data with the staff and together they challenged more of the steps and handoffs. Once they agreed there was no value in many of the steps the staff was onboard. Instead of feeling threatened they said, take me out of the process. They had never been clear on the value of these steps in the first place. They were often simply responding to email requests.

THE IMPROVEMENTS

Using the analysis and the insights from the Process (Gemba) Walk the team came up with solutions to reduce processing time and bring clarity to the process.

To reduce processing time:

- Eliminated the supervisor approval

- Reduced handoffs between groups

- Eliminated the need to send the form to the agency

To bring clarity to the process the form was updated with additional information:

- The person responsible for each section

- A list of Stakeholders

- A link to the new Standard Work

- A dropdown list of the cost center type being created

THE RESULTS

Over the course of four months the team tested their solutions. By eliminating the non-value added steps and handoffs, the process of adding a new cost center went from an average of 7 days to 4.2 days. And there were no more tales of customers waiting weeks or months.

WHAT'S NEXT

During this four-month period, Megan was surprised to learn that some of the accountants were continuing to send the form to be reviewed by their supervisors. The same review step the team had eliminated. It turns out they simply forgot the new Standard Work. Once they were reminded of the new process and provided with the link to the new form, the process continued smoothly.

This is not uncommon in operations like the FBOD. Staff work in numerous processes and if they haven’t processed a cost center form in a while they could easily forget or revert to old habits. Realizing this, Megan plans to check on the process periodically to see how it’s going and perhaps look for further improvements. She’s on a journey to seek perfection!

Megan Rulien is an Administrator at King County Finance and Business Operations Division (FBOD) working in the Financial Management Section. She’s part of the Lean Six Sigma program. Previously she worked as a research technician testing the safety of vaccines using non-human primates as a model.